What does PITI mean? PITI mortgage calculator

Contents

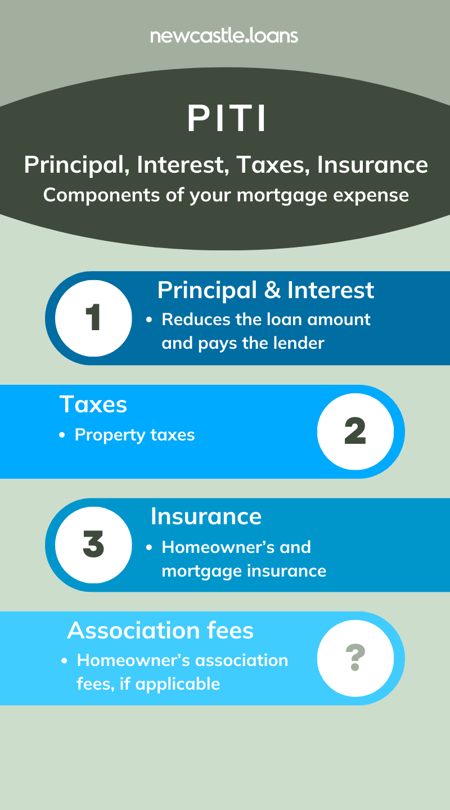

PITI stands for Principal, Interest, Taxes, and Insurance. The term refers to the components of your monthly housing expense.

What PITI means

PITI is your monthly housing payment of principal, interest, taxes, and insurance.- Principal is the money you borrow from a lender to purchase a property. Each month, a portion of your mortgage payment goes toward paying down the principal, reducing the overall amount you owe.

- Interest is the cost of borrowing money, expressed as a percentage. The interest is the lender's fee for allowing you to use their funds. In the early years of a mortgage, a more significant portion of your monthly payment goes toward interest.

- Taxes are the property tax you must pay on your home. The lender may collect property taxes as part of your monthly payment and then pay the taxes on your behalf when they come due.

- Insurance refers to the homeowner's and mortgage insurance. Lenders typically require homeowner insurance to protect the property against damage or loss. Additionally, suppose you make a down payment of less than 20%. In that case, you must pay for private mortgage insurance (PMI) to protect the lender if you default.

Some properties, such as condominiums and townhomes, may also include homeowner association (HOA) fees. HOA fees are part of the PITI. Together, these components make up your total mortgage payment.

What are HOA fees?

Homeowners Association (HOA) fees are recurring charges homeowners pay to an association to cover the costs of maintaining and managing a community or development.

Expect to pay HOA fees when you buy a condominium, townhouse, or single-family home in a planned development. These fees contribute to the upkeep of common areas, shared amenities, landscaping, security, and other communal services.

HOA fees vary depending on the property, location, and amenities.

Two Chicago condos are selling for $500,000. The HOA fees are $1,000 monthly for a highrise with a door attendant and a swimming pool in the Streeterville neighborhood. In contrast, the HOA fees are $300 monthly for a self-managed condo in a four-unit building in Chicago's Andersonville neighborhood.

- Review the Sales Contract Explainer to understand the terms and phrases in the real estate sales contract, like Homeowner's Association.

You pay HOA fees to the homeowner's association or management company, not the lender. However, the lender includes HOA fees as part of your PITI when calculating your debt-to-income ratio to determine whether you can afford the housing payment.

After you apply for a loan, the lender will send you a Loan Estimate. You will see the PITI in the Projected Payments section on page one.

Is the PITI the same as the monthly amount I pay the mortgage lender?

The PITI (Principal, Interest, Taxes, and Insurance) is not always the same as the monthly amount paid to the mortgage lender.

The PITI is a breakdown of the components of a mortgage payment the lender uses to determine if you qualify for the loan. In contrast, your mortgage payment is the monthly amount you send to the lender.

Your mortgage payment always includes the principal and interest portions of the loan, which go directly toward repaying the borrowed amount and compensating the lender for providing the funds. However, your mortgage payment may or may not include property taxes and homeowner's insurance, depending on your loan agreement,

Most first-time homebuyers have a lender-managed escrow account. When you escrow with the lender, your monthly payments include property taxes and homeowner's insurance. The lender holds the funds in the escrow account and pays the bills when they are due.

Some homebuyers waive the lender escrow and pay property taxes and homeowner's insurance separately to the relevant entities.

For example, I waived the lender escrow on my mortgage. Each month, I pay the lender principal and interest. Then, I pay the county property tax bills and homeowner's insurance premiums when they are due.

While the PITI represents the overall structure of the mortgage payment, the specific amount you pay to the lender might consist of the principal and interest, with taxes and insurance being paid separately by you or included in the lender-managed escrow account. The breakdown can vary based on the loan terms and agreement.

How do you calculate PITI?

To calculate your PITI (Principal, Interest, Taxes, and Insurance), follow these four steps:

Let's say you plan to buy a $350,000 Chicago condo with a 5% down payment using a 30-year fixed-rate mortgage at 7%.

- Purchase price: $350,000

- Down payment: $17,500 or 5% of the purchase price

- Loan amount: $332,500 or 95% of the purchase price

- Interest rate: 7%

1. Calculate the principal and interest.

Use a mortgage payment calculator to get the monthly principal and interest payments.

| Loan amount | $332,500 |

| Interest rate | 7.000% |

| Loan term | 30 years (360 months) |

| Principal and interest | $2,212 |

2. Estimate the monthly property tax.

Yearly property taxes are typically 1%-to-2% of the sales price, depending on the property type and location. For a house in Chicago, estimate the tax bill by multiplying the sales price by 2%. Then, divide by 12 to get the monthly property tax payment.

| Sales price | $350,000 |

| Annual property tax | $7,000 |

| Monthly tax | $583 |

| $350,000 Sales price x 2% Annual property tax rate = $7,000 Annual tax ÷ 12 = $583 | |

3. Estimate the monthly insurance.

Homeowner's insurance (HOI) is usually between 0.15%-0.5% of the loan amount, determined by the property type and condition. Estimate the premium for a Chicago condo by multiplying the loan amount by 0.15%.

| Loan amount | $332,500 |

| Annual HOI | $499 |

| Monthly HOI | $42 |

| $332,500 Loan amount x 0.15% HOI rate = $499 Annual HOI ÷ 12 = $42 | |

Private mortgage insurance (PMI) is required when your down payment is less than 20% of the purchase price. The amount varies based on several factors. For now, estimate the annual cost at 0.5% of the loan amount.

| Loan amount | $332,500 |

| Annual PMI | $1,663 |

| Monthly PMI | $138 |

| $332,500 Loan amount x 0.50% PMI rate = $1,663 Annual PMI ÷ 12 = $138 Monthly PMI | |

4. Add the principal, interest, taxes, and insurance.

Don't forget to include the homeowner's association

| Principal and interest | $2,212 |

| Property taxes | $583 |

| Homeowners insurance (HOI) | $42 |

| Mortgage insurance (PMI) | $138 |

| Homeowner's association fees (HOA) | $0 |

| PITI | $2,975 |

Use our interactive mortgage calculator to view current rates and payments, including estimates for property taxes, homeowner's insurance, and PMI.

Mortgage payment calculator

A mortgage payment calculator is a simple tool that helps you determine your total housing cost. Enter the purchase price, down payment, and interest rate. It computes the monthly principal and interest payments.

$0

$0

$0

$0

Our interactive mortgage calculator is a better tool. Use it to view current mortgage rates anytime from anywhere for a more exact PITI payment breakdown that includes the following:

- Principal and interest at today's interest rate

- Estimated taxes and homeowner's insurance

- Mortgage insurance quote

See the closing costs upfront on our website, too. Then, feel confident about buying a home because you know what to expect.

Check out our interactive mortgage calculator by clicking the button below.